Strategy & Leadership for the Replacement Economy

© Doug Macnamara, CMC & ICMCI

How many televisions/screens do you have in your home? How many additional will you buy?

- Will your next vehicle be larger, smaller or same size?

- Do you go to Tim Horton’s/Starbucks/Cafés more often, or are you eating more from home?

- Are you using more/less energy (electricity, gas, etc.) today than yesterday? Tomorrow?

- Do you donate to more or fewer charities today vs. 5 years ago?

- When did you last buy off the internet vs. going to a retail store?

- Does your 20-something relative have the kind of job they expected at this stage of career?

- Does your organization use more, less, or same amount of consultants?

- Can your government (federal, state or municipal) rely on the same level of corporate profits/average personal income to generate the same tax revenues as in the past?

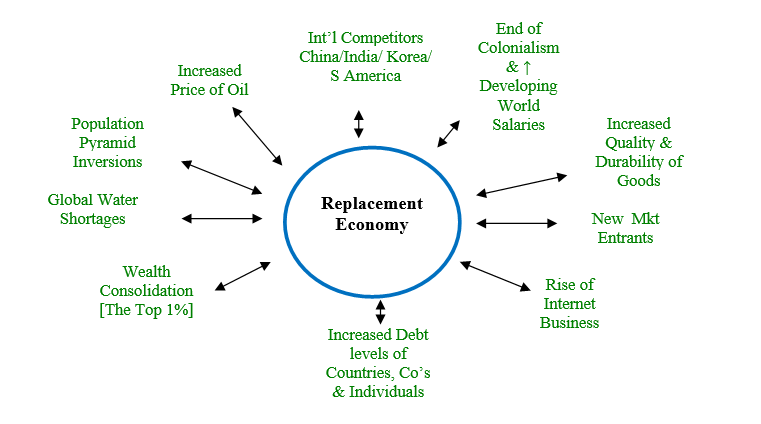

We are now well entrenched in what I call the Replacement Economy – Now, more than ever, it requires bold yet different strategy and leadership approaches than the growth economy of the past.

The End of Growth? Possibly, But Also Major Shifts and Re-Thinking Required

"Growth" has been the mantra of all my years in business, volunteer service and personal/family living. Indeed it has become so inculcated over the past 40 yrs within North America plus Asia and somewhat in Europe; that we don't even stop to think about the underlying tenets that created growth economies after WW2:

Imperialism/Commonwealth – dominant cultures drew wealth, raw materials & inexpensively produced goods from geographic or economic colonies;

- oil & energy-driven increased consumption with rising prices of fuel, new creation of drugs and therapies, new household materials, fertilizers and other petrochemical applications;

- enhanced durability and quality of goods that have extended product lifecycles;

- rising debt levels of, well, everything; and more. Today we are quite literally, reaching our limits.

Indeed, somewhere around 7 years ago we slipped, somewhat imperceptibly, from a growth economy into the Replacement Economy.

Here are some examples of these components, each of which could be worthy of a newsletter focus of its own.

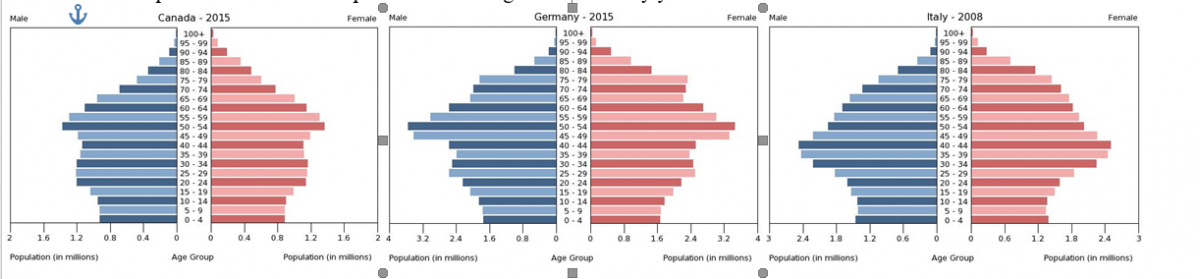

Population Pyramids

“Demographics is Destiny” claims Canadian demographer David K. Foot. Growth populations are those where the numbers of younger people outweigh the numbers of older people. The “up and comers” tend to have disposable income, and will spend money to establish homes, purchase furnishings, cars, etc. – assuming they have jobs that generate disposable income. ‘Western” countries typically have an inversion of their demographics where the older age groups out-number the younger age groups. This means that there will be less economic spending by following generations than the previous generations and a “stalling” of the economies. Western and Central European countries have experienced this stagnation for many years now.

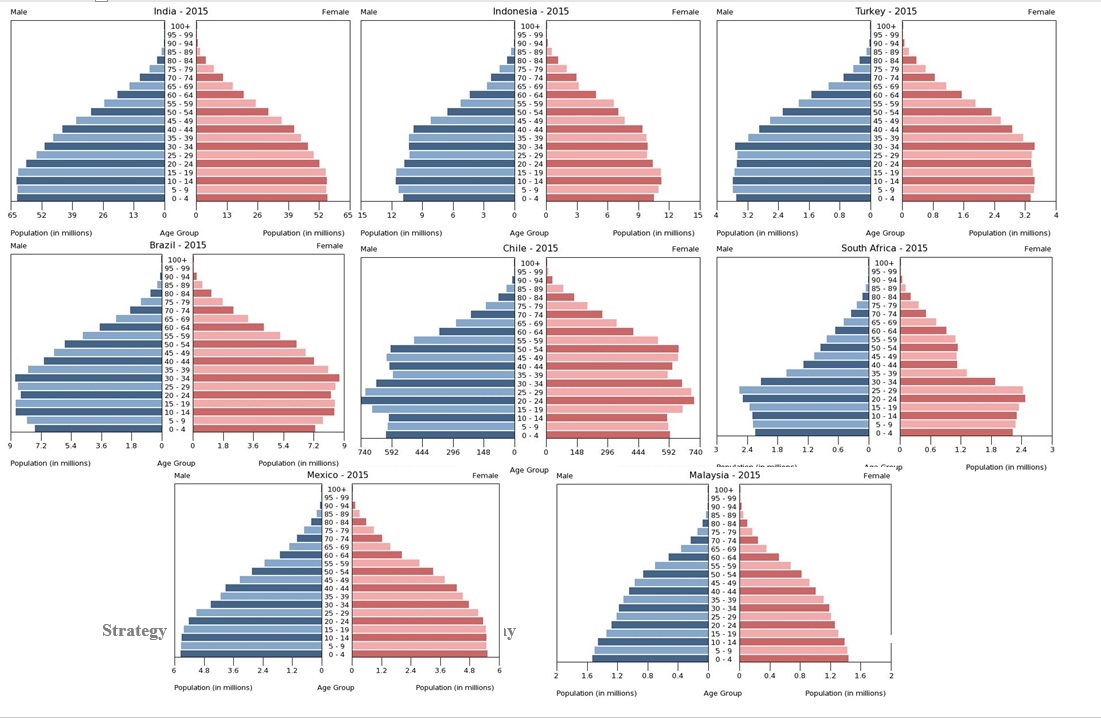

Asian, S. American and Arab countries all show significant populations of youth to drive their economies forward in the next decade or more. However, they must also be able to create meaningful jobs that can generate wealth and disposable income to drive purchasing power by the Gen Y/ Echo/ Millennials (median age 25) generation.

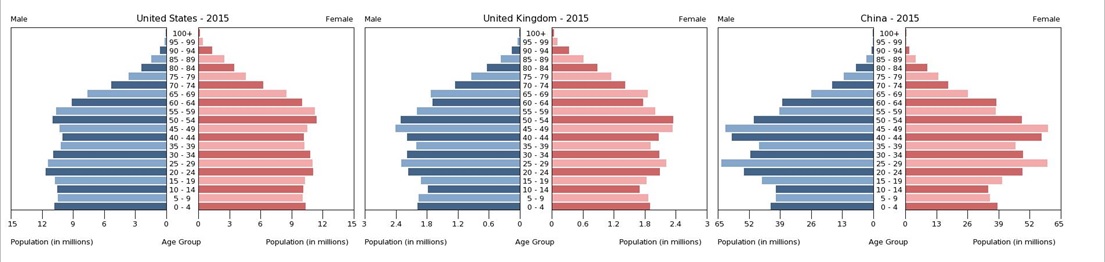

A few key countries through either Policy (China’s one-child policy) or immigration, have found ways to be anomalous to the above trends, flattening their pyramids, including USA, UK & China.

Looking forward, we can see a replacement of the “western” established economies as the dominant growth economies, by the truly growth-oriented developing economies. Key countries such as USA are driving their maintained demographics with the immigration of largely Mexican-origin citizens. UK has for some years fostered the immigration from many previous colonies and developing states. China has largely offset their potential for a growing younger demographics and can look forward to a decline in domestic growth from population.

China, Indonesia, India and Brazil are now emerging as the more dominant growth economies of the world, essentially replacing the traditional European and American economies. Strategy must take account of demo-shifts.

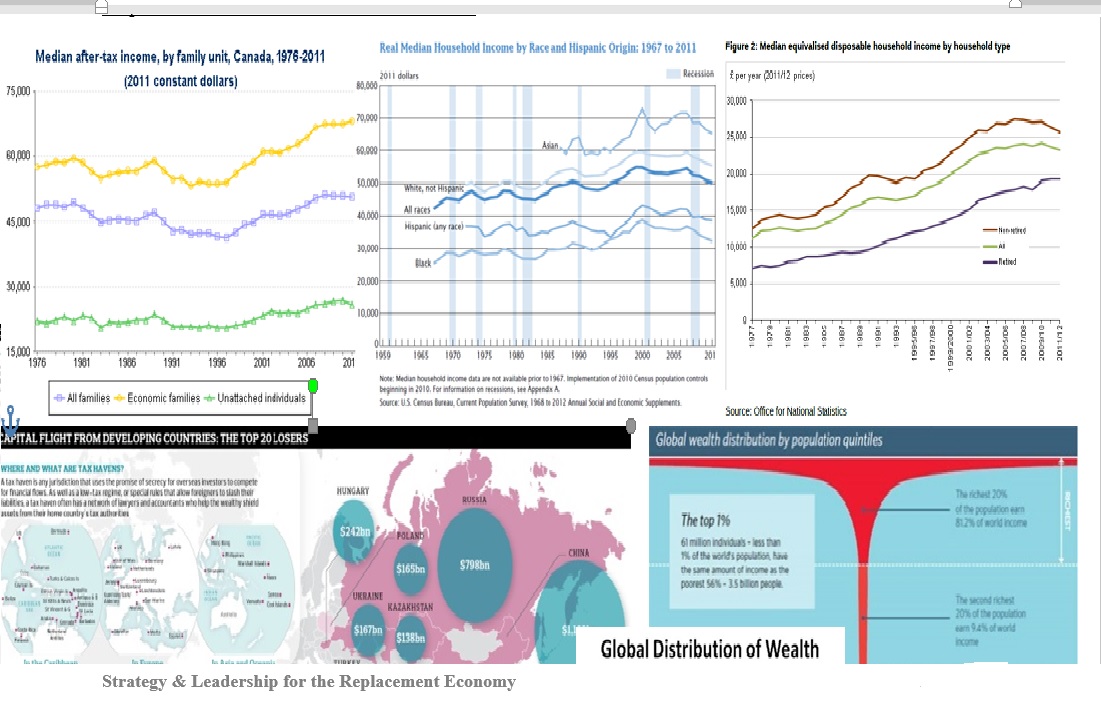

Disposable Income & Concentration of Wealth

The first set of charts above for Canada, USA and UK, show that for median families, the past 20+ years have been marked by marginal disposable income growth, meanwhile the top 1% have consolidated their wealth, and in many cases sought offshore tax havens to squirrel-away their wealth. The old axiom of capitalism “the rising tide will raise all boats” has clearly not actually happened. This has meant more and more difficulty for the main sections of populations to increase their purchasing power, and drive-up the economy in a sustained manner.

Disposable income in Western countries has remained largely flat, and in several European countries has seen decline. At the same time, many more options for how & what to spend our money on has exploded – with global distribution and global brands getting products and even services to almost every corner of the world. This means that in most countries/communities traditional sources and products are being replaced by international competition. Traditional recreational pursuits, family activities & household expenditures are being replaced.

The concentration of wealth into the top 0.1% of the global population (forget about even the 1%!) is enormous. Government policies, regulation and laws have completely failed to produce some semblance of fair distribution of the overall rise of wealth in the world. The above global chart shows that some 91,000 individuals from the 20 lowest developing economies have put $10 Trillion into private offshore bank accounts is particularly egregious.

Without measures to spread the wealth at least somewhat, there is no money amongst the masses to spur consumption and growth whatsoever into the future. The rich keep getting richer, and the rich-poor gap widens.

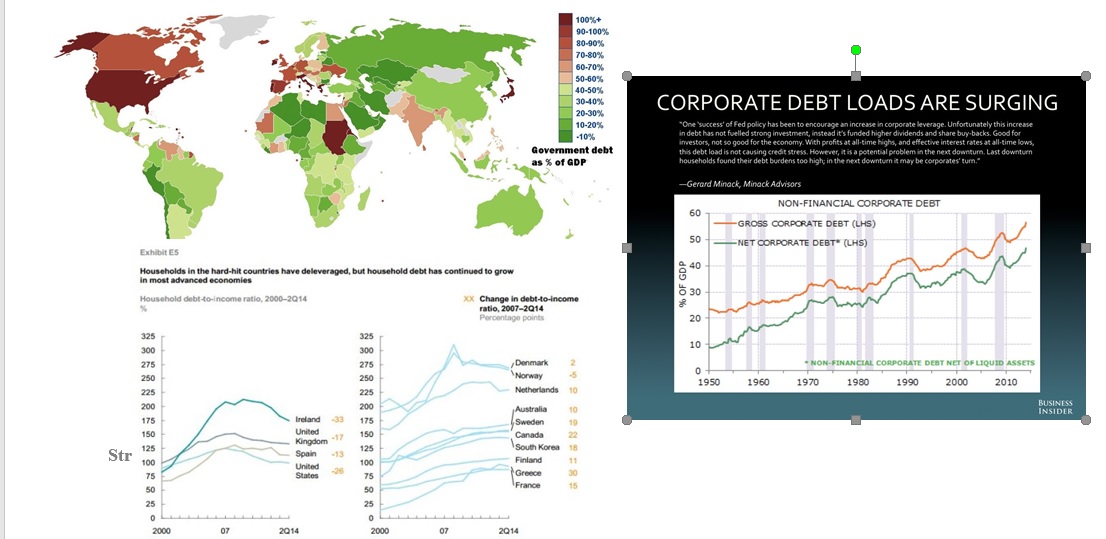

DEBT Everywhere!

Of course, through the 2000’s, the answer to sustaining the ability of the masses to keep purchasing ‘stuff’ was solved by providing ‘easy’ loans to consumers for houses, cars, everything. Several national governments created low corporate tax zones to attract business. These factors led to the first major recession of 2008-10 caused by sub-prime mortgage crisis, bank failures, and the PIIGS sovereign debt crisis in countries of Europe. When the recession did not rebound as expected, the USA, Canada, and more recently European Union (after Austerity didn’t work), started their quantitative easing programs – essentially printing more money and racking-up significant national debt.

We now have the highest levels of country/state, corporate and personal debts ever. If that doesn’t cause people to start spending their money more carefully and slowly, pulling back on growth, then what will? Debt repayment has to replace purchasing of discretionary goods and services. Meanwhile, many Asian countries have been more careful with their debt levels and again replaced the traditional purchasers of debt, such that China and others are now the biggest creditors to traditional power countries and companies.

Combined with aging Boomer generations and their need/focus on health care, this means also that there is less of disposable income, corporate & government resources (after debt repayment) for other things such as:

• donating to charities (donors are replacing multiple donations with ‘select’, scrutinized donations),

• raising salaries (lower annual increases replaced by performance-related increases),

• providing scholarships for education,

• funding of social services (both education & soc services, replaced by need for medical/health funding).

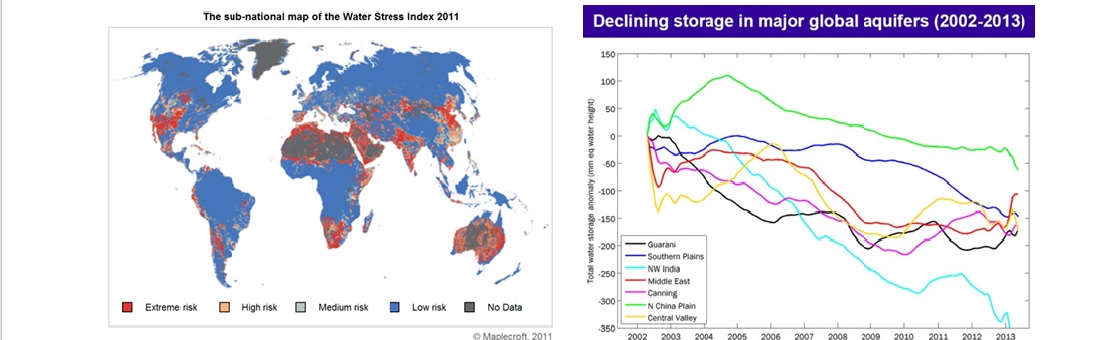

Water Table, Aquifer and Reservoir Depletion

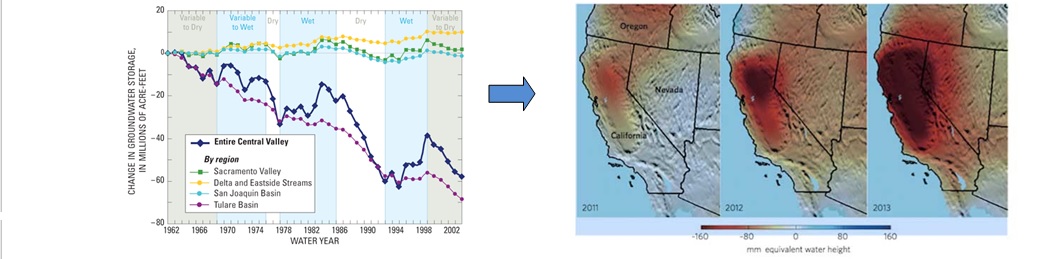

As one example of the critical state of depletion of many different resources; for decades now, major water tables around the world have been depleted at a rate faster than they can be naturally replenished. When the regular water table runs low, we tap the next deeper aquifer and look for new water by drilling deeper wells. Agriculture to feed rising populations , the increase the % of protein (vs grains) in diets around the world are both diverting more and more water. Bio-fuels and water for oil drilling, fracking, oil sands reclamation, etc. have also used up precious water and replaced “normal” agricultural use of water.

Water depletion will and already is causing us to replace previous priorities for water use. As late as 2014, the state of California had NO regulations and policies about who and for what purpose, people and companies and governments could access water. They had a poor sense and understanding of their natural bounty of freshwater. And when weather patterns shifted – only then did the real state of this precious resource become apparent.

California has been particularly hard hit with drought recently, requiring new legislation being urgently put into place on the fly after virtually no policy ever restricting water use. Gardening and grass watering is being replaced by water priority for agriculture, and growing city drinking water needs. Maybe we will need to make further priority choices as well.

Increased Durability and Quality of Goods.

According to a recent Forbes article, the age of the average vehicle on the road in the US is 10.8 years! This is up from an average of 7yrs only a decade ago. Car purchase financing of 7 year loans is now commonplace. While this quality improvement is a good thing, improved lifespan of goods means slower growth, a longer replacement lifecycle and slower use of resources. Now, the reason for buying a new article for your home is not likely due to functional obsolescence. Instead, replacement will be due more to new innovations, design changes or accidents/breakage. Also there is an evolving trend for hardware (beyond the computer industry) that is ever more durable, with hardware builders supplying software updates able to change/improve the hardware performance or experience. From computers to vehicles to smart homes and more, software or smaller add-ons are increasingly being used to upgrade the durable base item with refreshed or upgraded experiences.

Baby Boomers (still the dominant segment in western countries), have today purchased all the numbers of things they will ever need. They don’t need to buy more stuff – just replace old stuff, on a slower pace than before.

The younger Millennials are buying increasing goods of course, as they establish careers and households, however, many do not have the same values – they value quality experiences over “stuff”. Many are either forced to or are choosing to live with smaller footprints. And, as illustrated above, there are fewer Millennials than Boomers. In Asian, Indo-Arab, and Central/Eastern European, African and S. American developing economies, the next generations will likely be forced to ‘live small’ simply because there aren’t enough resources on the planet to support 1/3 the population of China OR India to achieve the lifestyle and quality of life Canadians enjoy.

Living Small will have to replace Living Large.

Increased Scarcity & Price of Oil Drives a Decline of Growth

In his book The End of Growth, Canadian economist Jeff Rubin makes a compelling argument for the connectivity of Energy (more particularly the price of Oil) to GDP. Rubin asserts that, as the price of oil goes up, so does GDP. As supply goes up and oil profitability rises, so does GDP – to a point. At some point, increasingly scarce and more costly to extract oil, causes the supply to level-off and or turns the growth of profitability negative. In parallel, as the price of oil goes up, at some point triple-digit price per barrel becomes unaffordable and unsustainable. “We can’t continue to increase our energy utilization exponentially… [Also] when we stop finding sources of oil/energy, our economies stop growing.”

In his book The End of Growth, Canadian economist Jeff Rubin makes a compelling argument for the connectivity of Energy (more particularly the price of Oil) to GDP. Rubin asserts that, as the price of oil goes up, so does GDP. As supply goes up and oil profitability rises, so does GDP – to a point. At some point, increasingly scarce and more costly to extract oil, causes the supply to level-off and or turns the growth of profitability negative. In parallel, as the price of oil goes up, at some point triple-digit price per barrel becomes unaffordable and unsustainable. “We can’t continue to increase our energy utilization exponentially… [Also] when we stop finding sources of oil/energy, our economies stop growing.”

The short or medium term price decreases for oil due to market gluts as we are experiencing in late 2014/2015, are occurring simultaneously with a global slow-down of production and utilization of oil, having the same effect as above… leveling off of GDP and the end of several growth economies. It’s clear that the slowdown in this case is not due to rising oil prices. Instead, the slowdown is likely caused by the other “pull” factors above.

Rubin does a masterful job of showing the complex network of ramifications and implications of just this one dimension of energy and particularly oil on the generalized slowing of growth in Western societies.

The impact of slowdown across Europe and the Americas is also reaching into South America. Asia, classically the producers of goods for the Western economies are scaling back to adjust. However, if Asia can get their expansive middle class to start spending, countries like India, China, Indonesia and others can develop strong internal markets and GDP growth.

So what? With all these trends contributing reduced growth and/or the new replacement economic dynamics, what does this mean for organizational strategy and leadership?

Strategy for NEW Realities

Systems-Network View for Sustainability

Within an overarching context for slowing of growth, one has to start into Strategy thinking and planning with a clear understanding of some key principles:

- First, this is a complex, system of systems (network) exercise. You must lift yourself and your fellow executives and Board members out of Analytical, single dimension thinking based upon past parameters; to at least a Systems-level… understanding the multiple relationships and interdependencies in your marketplace, your industry sector and your company; or more preferably to a Network-level… understanding dynamics in the various markets that you touch and that impact your organization, seeing and recognizing shifts in preferences and replacement decision-making by customers/clients, plus ‘flow’ of the movement within the marketplace and your network; to sketch out where and how you want to be positioned amid these dynamics 5-10 years from now. Simplistic, inward thinking won’t cut it anymore.

- Within a general flow towards the end of growth in western societies, the various elements outlined in the first section will all impact YOUR situation differently from others. Canada, the US, Western and Central Europe may all be trending towards stagnation; but there are and will be regional differences. Some traditional businesses will have future opportunities very different from some of the new businesses. Some health charities for example may well be more attractive to older boomers, vs. international aid and development charities attractive to idealistic, well-travelled, culturally less-biased Millennials. Even within a general inverted population pyramid of Canada shown above, the regional dynamic of Alberta is very different from the regional dynamic of British Columbia as shown below. Success is still very possible in all conditions.

Clearly Alberta, and Edmonton in particular, has a very significant Millennials group – bigger even than the Boomers cadre to drive a future growth-potential economy; whereas BC, and Victoria in particular, skews older with a more modest Millennials replacement-potential dynamic. And this is only ONE dimension variance! The same type of business based in Edmonton must make different strategic choices compared to that of the Victoria-based business.

- Now, I know this is heresy; but we really need to re-think our default assumption that Strategy is only about how to sustain growth and improve profitability of one enterprise – and, measured only in financial terms. This thinking is being replaced (out of crisis, or necessity, or enlightened understanding) with more of a focus on sustained Value provision and sustained moderate Profitability, plus sustained moderate ROI. Perhaps we can also consider measures of social stability and wellness as well as environmental wellness – the Triple Bottom-line so to speak. This won’t win fans of asset-growth investors with this focus, nor is it the best assumption for our personal retirement funds; but it is becoming clear that new investment approaches and assumptions are needed to replace traditional ones. Perhaps what we look for are sustained profit sharing and year over year dividends of say 5% rather than capital growth. This might just be the most sustainable way into retirement anyway! In and of itself, 5% annual profitability is going to be incredibly demanding of continuous innovation and productivity in our replacement economy.

- Take time to strategically think, look at the various dynamics in play around your organization and marketplace/community. Consider various options for replacing existing products, services, programs, experiences with new ones “tuned” for the evolving dynamics and where you can position yourself to create value 5 years from now vs. yesterday. Really think carefully and thoroughly: what will be of value in 5 years to your clients and what they will be wanting from you plus where you might innovate new offerings? Assess where you need significant improvements in productivity and cost control design of workflow. Then you can break it down in a planning approach – setting Goals, Outcomes Measures of Success and building strategies.

- Wherever possible, try to eliminate emotional decisions or position-taking based upon historical assumptions, “good old days” thinking and traditional politics/values; Now more than ever, we must focus on future, shift changes within customers and marketplace, and new dynamics , value flow and competitive replacement services and products.

Some other axioms to explore and truly understand in a network perspective:

Profits/Surplus = Reinvestment & Sustainability (You NEED to generate surplus whether

in the for-profit, NFP or government sectors.)

Employment = Customers for products & services (We can’t cut our way to broad prosperity)

Part-time jobs, job sharing, jobs for seniors, mentoring jobs, etc. – We should be thinking MUCH more strategically about jobs and the jobs dynamic to ensure we still flow money in an economy and still have customers capable of buying our products/services.

Innovation = Replacement offerings of value and market share sustainability/capture.

Productivity = Increased standard of living + protection of finite resources.

Important Dialogue, Trade-offs, Policy & Priority Setting

Let’s take the example from above of the depleting water tables and aquifers outlined in charts.

Water is already an international, national and regional issue – where there has been little serious dialogue and debate around priorities, relative values, who owns what, and the “best use’ of this incredibly valuable but shrinking resource that we take for granted.

Should we use freshwater to prop-up dying resource extraction businesses or industries where the growth is levelling off? If we are going to transport water anyway, could we more appropriately use sea water to inject into oil/gas wells and use fresh water for agriculture?

Should we use freshwater to prop-up dying resource extraction businesses or industries where the growth is levelling off? If we are going to transport water anyway, could we more appropriately use sea water to inject into oil/gas wells and use fresh water for agriculture?

If we use fresh water for more agriculture, what priority crops or utilization should we have? Who owns the water?

- Where we have some abundance and easy access/transportation of water, maybe we should use it for more valuable protein production which can then be shipped internationally and generate higher profitability – to regions of the world where scarcity of water should prioritize its use for, say, drinking.

- This has application to replacing our past low-value business strategy of just bottling and shipping the basic water, to a more high-value intellectual capital leveraged replacement product.

- This also has application to public policy-making and relative industry support programs at the regional government level, plus also regulations and monitoring. Maybe while we pump oil in one direction through a pipeline clearing, we can also pump sea water in the other direction to support the extraction of oil at the source. Maybe the seawater pipeline can have a “safety” and “contingency” catchment & containment design for if the oil pipeline should develop a leak?

- Although we have lesser Policy challenges than the Nile River flowing through multiple African countries; within regions we might build policy and priorities around who and for what purpose and what amounts can siphon off our river water. This should be done with an eye towards favouring future high-value usage vs. support for industries already far down the replacement dynamic. Of course this will be controversial, and also necessary.

- Consumption (of oil, protein and other processed food, water, knowledge products) is going to be skewed into the future towards emerging countries/economies and away from the developed countries/markets. What might your organization do strategically, to access these new markets?

- Waste creation, pollution and carbon/toxic gases released into the air are also skewed to these developing countries/markets. Cradle-to-grave product life-cycle management is going to become ever more a strategic consideration in all regions and industry sectors of the world.

- Government taxation assumptions need to adapt very quickly from the default assumption of growth business and growing citizen disposable income, able to pay continually rising taxes. This is not sustainable in stagnating and replacement economy dynamics. Governments need to re-prioritize its work, seriously think through how to replace its own value proposition delivery elements, and cut-back on old and outdated policy/programs- reducing costs of government.

What will you STOP Doing?

One of the most important strategic considerations for senior leaders and their Boards/Government Cabinets, is what to STOP doing – so you can redirect limited resources towards replacement initiatives and priorities. What will your business, government department or NFP STOP doing in response to the replacement economy dynamics?

Leading for Innovation, Productivity, Value Extension

Important to today’s replacement economy is Innovation & Productivity – two sides of the same coin. However, few understand what it actually takes to facilitate this effectively. Most innovations do NOT come from Research, especially in Universities or Centres of Excellence (only about 30%). Similarly, most productivity improvement does NOT in fact come from automation or IT solutions. The roles of professionals at the front-lines, as well as in Operations/Sales/Client Service Management generate 70%, and are critical in ensuring that innovation and productivity initiatives lead to enhanced value of products and services – and that they deliver bottom-line results. Of course research groups and marketing departments can and should also contribute to innovation as well.

Back to Jeff Rubin’s book again, The End of Growth, Chapter 8 looks at both the concepts of “Zero Sum World” and “The New Consumer” – largely from his oil price perspective. This is equally valid and well argued. As Rubin points out; “In the 1980’s, China’s oil consumption was 2 million barrels per day. Today its consumption is verging on 10 million barrels per day…In a zero sum world of global oil supply, China’s demand for fuel will come at the expense of say, the United States.” “Americans consume roughly 20 percent of global oil production, while producing less than 10 percent. That’s a big gap that the US currently bridges from importing oil from foreign countries. If China’s economic growth continues to outpace the United States’, China will gain competitive advantage for more barrels.” Western economies with declining populations and/or GDP will be competing in the future with developing countries and their growing populations/GDP for everything from oil to water to steel to wood, rare earth metals in electronics- everything!

The new consumer meanwhile, particularly from the millennial generation, is starting to embrace living small. Living small does not have to mean lower standard of living – just different. This generation is already showing preponderance to valuing experiences over stuff…..

All of these trends suggest that organizations geared towards innovation of new products and services, plus focused on improving productivity, are going to be the organizations that replace others not oriented this way, in market share and customer connection. Innovation and Productivity simply must become important components of future strategy. Even those in the NFP context and government departments/agencies will need to adopt innovation and productivity – plus the ability to show tangible positive impact on the community using fewer resources.

Innovation for Value Creation

In a world of frugal spending, more durable goods, massive choice from amongst global competitors, an incredible global distribution and shipping network, access to knowledge and experience through inexpensive web-based communications, and more sophisticated customers with personal social media networks of influence and reporting of bad players; the very essence of leadership must embrace the ability to facilitate innovation towards specific and measurable pay-offs and profitability.

This starts with investigating client/potential client needs and/or problems – often not well enunciated by the client/potential client. Getting out to observe your clients in action, and building relationships with them directly (face-to-face or using technology/media) becomes critical to generating innovation ideas. Solving Customer Problems has proven to be just about the ‘best’ challenge for successful innovation. If we can identify a customer problem or paradox – Innovation can work on that tangible issue and generally find success. As a leader, you must be part of the active exploration, identification and narrowing of focus of the innovation efforts. You can’t demand this of your people then walk away.

Facilitative leadership, collaborative problem solving, pattern-connecting, and product/service strengthening are important leadership skills for the replacement economy environment. Following on from here is the ability to champion its potential for investment funds to be apportioned, then tenacity to marshal people and system resources to build and reliably deliver the promised solution. Finally there is the sales and marketing process – into both existing clients and new, untapped markets/clients with the innovation – delivering payback of the investment within the initial or early second cycle of its creation. Very demanding. Very important. Very different, from a habitual growth market dynamic.

Hardware vs. Software vs. Combined Innovation

What the computer, cellphone and ‘pad’ revolutions have shown, is that simple hardware development and sale is not enough. Even with consumer product replacement life-cycles of 2-3years; software updates weekly, which improve the features and experience of the hardware, are incredibly important and linked.

Now however, this expectation has become so ingrained, that consumer expectation is that this will be a part of not just electronics products – but all products and service areas including homes, vehicles, sports stadiums, offices, even outdoor adventure – all should be finding ways to embrace software-updateable experiences.

The Replacement economy moniker thus has yet another connotation; regular replacement of content, and features and applications through software upgrade as the expected basis for sustained value proposition. Even as product replacement cycles may lengthen towards say a 4year cycle or longer on more expensive items; expectations for continued upgrading of value by customers will need to be built into your innovation thinking and processes.

Upgrade/Extension vs. Replacement

If low or no growth becomes particularly well established, then consumers may even go further eschewing replacement of capital investment products on a much slower cycle, and expecting or shopping for “upgrades” and or “add-ons” or base hardware “extensions” as a basis for sustained relationship and value attachment to the original product purchase. Living small may become reality, but still people will aspire to living with regularly improved performance of purchased items. Again, think how this might apply to your business, homes, cars, tourism, offices, employment, education, consulting services, Charity donations, Government services, and more.

Product vs. Experience – Value Proposition Design

If changing attitudes towards buying stuff is replaced significantly with buying experiences, then every innovation needs to consider not just the item itself, but the customer’s experience of the item. The future added value experience of the item may actually be replaced with the purchase of just the experience, and not even purchasing items at all.

Interface corp (carpet company) realized several years ago, we aren’t really buying a carpet or rug for my floors, I am buying the experience of having clean, warmth-inspiring, “cozy” experience of coverings on my floors. The product manufacturing and single sales strategy assumptions “growth of units of carpets sold”; is replaced instead with the concept of selling contracts for fresh and cozy experience of the home environment – with a regular profitable service/software/modular update income from a long lasting relationship with the client. If a stain or tear in the carpet occurs, the service provider replaces a carpet tile to keep everything looking fresh and new.

In a public policy sense, should a regional government build policy based on supporting the sale and export of ever lower-margin “stuff” (measured in traditional GDP, and competing against perhaps lower labour-priced regions elsewhere in the world)? Instead, perhaps we should shift towards policies and programs that attract tourists looking for the “experience” of the uniquely beautiful, safe, natural, affordable, soul-stirring environment that can be sold profitably and supported over time with relationship enhancing and possibly repeat-visit inducing software-generated enhancements of the experience when they return home. What innovative experiences will your organization/team provide?

Productivity Improvement for Sustained Profitability and Standard of Living

Continued pursuit of efficiency and quality experience improvement, developed/delivered in cost effective ways, is not only the basis for enhanced competitiveness, but it is also the basis for sustained standards of living of employees and our communities at large. Just like Innovation on one hand, so too Productivity is critical on the other hand. This is not always well understood. [Financial Post article, May 22, 2015 by William Watson.]

Continued pursuit of efficiency and quality experience improvement, developed/delivered in cost effective ways, is not only the basis for enhanced competitiveness, but it is also the basis for sustained standards of living of employees and our communities at large. Just like Innovation on one hand, so too Productivity is critical on the other hand. This is not always well understood. [Financial Post article, May 22, 2015 by William Watson.]

Surprisingly few organizations ensure the following fundamentals of Productivity are implemented well. These are important leadership areas.

People: are your people focussed, motivated and effective? What is your turn-over rate? (Regularly having to recruit and re-train individuals really takes a notch out of your productivity.) How is your level of internal collaboration, information-sharing and appropriate involvement in decision-making? Do you have the right talent for the challenges at hand? Do they understand and focus on “advancing the business” of the organization?

Most importantly; do people truly understand what a highly productive 8hr day looks like, sounds like, feels like?! Do your employees understand what it takes for them to personally create “value” above and beyond their individual cost to the organization – every hour?! This is a concept that has been ignored by so many organizations and senior leaders for so long, that the average employee does not even know what they have to do/why it is necessary for them to create more value than their all-in costs to the org.

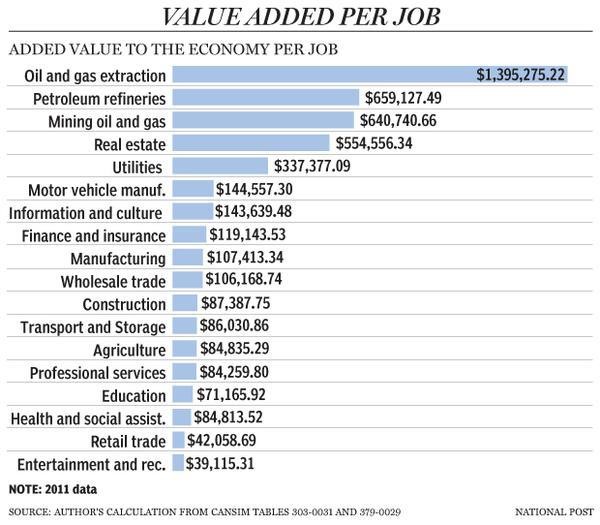

Recently in another article in Canada’s National Post, Trevor Tombe of the University of Calgary, and author of the book Better Off Dead: Value Added in Economic Policy Debates, presented this chart showing the value-added contribution of a selection of jobs in various industries.

Recently in another article in Canada’s National Post, Trevor Tombe of the University of Calgary, and author of the book Better Off Dead: Value Added in Economic Policy Debates, presented this chart showing the value-added contribution of a selection of jobs in various industries.

Unfortunately, just focusing on GDP gets us reacting to the chart in a biased manner. Entertainment and recreation (in chart on left), may score low in the GDP sense; however, they score high in the social cohesion & community stability area. These lower GDP roles also done in an intentional manner, might contribute to environmental sustainability and thus 2 areas of a triple bottom-line measure of community benefit. All jobs need to focus on the value-add they are contributing.

Org. Design: Are your people deployed in the best manner to deliver the customer service, programmatic impact or product appreciation you are working to achieve? “Form” really should follow “function”, and as the organization shifts its resource complement, its service evolution, and/or its relationship with clients/distribution partners/end-consumers; then so too we need to be able to flex the organizational design and job descriptions. Today it is not uncommon to adjust the org design annually!

Compensation & Reward Design: do your reward mechanisms support the new expectations of performance? Are your performance management (annual performance plan + annual performance appraisal) mechanisms in place and adjusted to be in-synch with the new work design and expectations? Are compensation/reward elements reinforcing the same expectations amongst everyone?

Technology & Interface: Perhaps the most under-appreciated element and often the biggest barrier to advancement, is the integration of technology with our human creativity and capacities. First, the technology just has to work properly! Second, the software and people interface has to support the org. design and desired new human/team practices. Third, technology has to help elevate performance and impact in the manner that actually has more value to the customer. Often technology can create more work for employees, and turn out marginal value to the client.

Executive Facilitation: Executives are an important part of productivity success. Employees often simply can’t ‘do more with less’ or figure out productivity improvement, when the senior leader simply demands it in staff meetings. Executives need to be on the front-line with staff to see and understand how the elements above are working together. Executives provide context and understanding to employees about why priorities and focus are the way they are. And often, executives must personally connect individuals, capture and champion good ideas, and/or bring clients, employees, and technology support people together to explore improvements. Indeed, executives themselves must have an ability to visualize what success might look like or include, and facilitate that exploration and solution building amongst employees and broader network players (suppliers, consultants, community, clients & partners).

Quality, LEAN, Six Sigma, Kaizen, BPR Processes: The use of these initiatives must be applied to the advancement of the organization towards their operational goals. Sometimes, projects in QI or BPR can take on a life of their own, and it’s not clear how they are actually advancing the organization – towards their goals! Executives must ensure that these initiatives are integrated within new org design and technology application and that they align with the new strategic/operational plans.

Reviewing your internal processes and applying LEAN, 6-Sigma and/or LEED methodologies will assist integrity of your product/experience, and allow you to constantly adapt and improve.

This is particularly important if you decide strategically to stop doing a particular line of business or service, replace it with a higher priority line, and seek to find innovative new value propositions for these changing global-regional dynamics. Both older and new processes should be regularly addressed with proven Productivity processes. Again, today’s senior lead must be capable in facilitating Productivity exercises/initiatives with their people and/or outsourcing to others with this expertise.

Both Innovation & Productivity can be creative processes. Both can be engaging, satisfying, collaborative, and profit-generating exercises.

In Conclusion:

In reality, the economies of Central and Western Europe, the USA and Canada and other closely aligned countries, have been living the Replacement Economy for more than 7 years. The global sub-prime mortgage debacle was the first significant and public signal that most of the Western world was living far beyond their means. This has been further exacerbated since 2012 with stimulus monetary policy and government debt-creation, first in the USA, then Canada, and more recently most of Europe – with even Germany now backing off its original Austerity approach. Now, individuals and families are also taking advantage of globally low interest rates to expand personal debt – with the non-mortgage debt being the most dangerous, if not offset by improved asset value. Oil is currently not driving GDP as it once did.

Most of the stimulus and debt accumulation has been done with an assumption that the current economic challenge is just something we have to ‘weather’ or get through. Then, once things are back on-track in a couple of months/years we will be able to pay-back the debts.

But what if this is not just a phase we are going through, what if this is actually the new normal? It’s been going for over 7 years with no signs of rebound yet! Indeed most of the factors described above suggest the Replacement Economy condition IS the new normal, and it will be next to impossible to repay the accumulated debt! Regardless of an eventual bounce-back, “normal” is not going to return anytime soon!

This means you, me and senior leaders of government/civil service, business and NFP’s must all re-think our current programs and services and roles in the community; replace the old-school/old-thinking priorities with new, more appropriate and value-generating initiatives that take account of our regional uniqueness conditions, and re-frame our strategies towards a new world order. Failure to do so, will not just be a failure of personal/organizational leadership, it will be failure towards our children and grandchildren, and communities at large.

Now; does anyone want to talk Strategy for thriving in the Replacement Economy?

Are you ready to vigorously pursue new areas of Innovation for new Value-creation?

Shall we get serious with our own personal, team, organization and societal Productivity in order to maintain jobs and protect our standards of living?

Status quo, is simply not sustainable, and likely means your organization will be replaced by a more innovative and higher productivity enterprise if you too don’t embrace these practices!

---------------------------------------------------------

Banff Executive Leadership Inc. offers strategic thinking/planning facilitation around the world, plus public and customized programming to improve Board Governance and Executive Leadership Practices. We also provide coaching and consulting services to Boards and Executives to help enhance their leadership practices. Please contact us if we can be of further assistance.

----------------------------------------------------------

If you found this article useful, please forward the article's web link to a friend!